Quick Answer

Catch-up bookkeeping is the process of bringing your financial records current when you’ve fallen behind — typically months or years of unrecorded transactions, unreconciled accounts, and uncategorized expenses. For most small businesses, catch-up takes 2–8 weeks and costs between $1,500 and $15,000 depending on how far behind you are, how many accounts and transactions are involved, and the complexity of your business. The longer you wait, the more it costs — but the sooner you start, the faster you regain control of your finances and reduce IRS risk.

Why So Many Business Owners Fall Behind

If you’re behind on your books, you’re not unusual — you’re typical. We see it constantly at Anchor: business owners who started doing their own bookkeeping in QuickBooks, got busy running the actual business, and woke up one day realizing they haven’t reconciled in 14 months.

The most common scenarios we see:

- DIY that drifted — you started in QuickBooks Online or a spreadsheet, kept up for a while, then life and business got in the way

- Bookkeeper turnover — your previous bookkeeper quit, got sick, or quietly stopped doing the work, and you only found out when tax season hit

- Software switches — you migrated from QuickBooks Desktop to QBO (or to Xero, or back) and transactions never fully imported correctly

- Business growth outpaced the system — what worked at $200K in revenue stopped working at $1.5M, and the books quietly broke

- Multiple bank accounts and credit cards added over time, with no one tracking which transactions were business and which were personal

- Major life event — a death, divorce, illness, or business transition pushed bookkeeping to the bottom of the priority list

None of these mean you’re a bad business owner. They mean you have a normal small business that’s grown faster than the back office could keep up with.

What Catch-Up Bookkeeping Actually Includes

Real catch-up bookkeeping is more than just “entering missing transactions.” Done correctly, it produces clean, tax-ready financials and a system that won’t fall apart again. Here’s what’s involved:

1. Discovery & Document Gathering

Pulling together every bank statement, credit card statement, loan statement, payroll record, sales tax filing, and prior tax return for the period being caught up. This step alone can take a week if records are scattered. We’ll typically request read-only bank access through QuickBooks Online to speed this up.

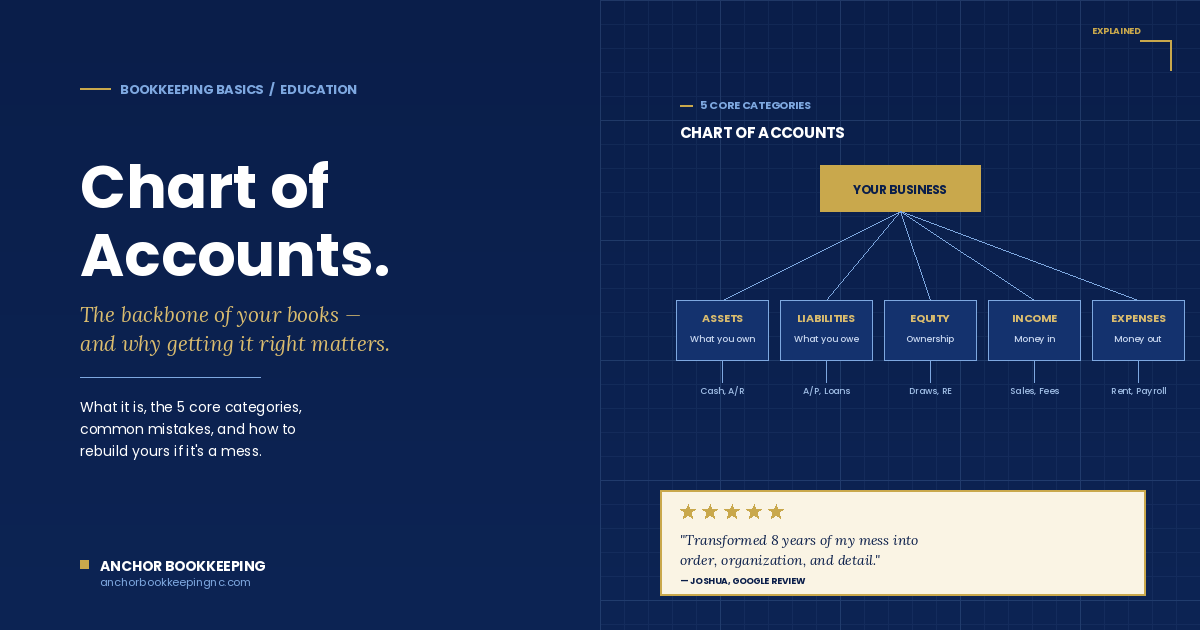

2. Chart of Accounts Review

Most catch-up engagements start with a chart of accounts that’s either too generic, too messy, or set up for a different kind of business. Before we enter a single transaction, we restructure the chart of accounts so the financials will actually be useful — meaning your P&L will tell you something about how the business is performing, not just satisfy the IRS.

3. Transaction Entry & Categorization

Every transaction in every account, coded to the correct category. For most businesses this means importing bank feeds, matching them to invoices and bills, and categorizing what’s left. The key is consistency — once a vendor is categorized one way, it should be categorized that way every time.

4. Bank & Credit Card Reconciliation

Every account, every month, reconciled to the statement. This is the step DIY bookkeepers most often skip, and it’s where errors hide. Reconciliation is what proves the books are actually accurate, not just “close enough.”

5. Accounts Receivable & Accounts Payable Cleanup

Reviewing open invoices and bills to identify duplicates, paid items that weren’t marked paid, and uncollectible balances that need to be written off. Most behind-on-bookkeeping businesses have an A/R aging report that’s full of fiction.

6. Payroll Reconciliation

Matching payroll provider records (Gusto, ADP, QuickBooks Payroll) against what’s actually recorded in the books, including payroll taxes, benefits, and 1099 contractor payments.

7. Sales Tax & 1099 Verification

Confirming sales tax was filed and paid correctly for each period, and that all 1099-eligible contractors were tracked. This step alone has saved Anchor clients from significant penalties in past engagements.

8. Financial Statement Preparation

Once everything is entered and reconciled, producing month-by-month P&L, balance sheet, and cash flow statements for the catch-up period — so you (and your CPA) can finally see the real picture.

9. Handoff & Forward-Looking System

This is the part most catch-up engagements skip. Getting current is only valuable if you stay current. We document the new chart of accounts, set up monthly close procedures, and either hand it off to your team or roll into ongoing monthly bookkeeping.

How Long Does Catch-Up Bookkeeping Take?

Realistic timelines based on what we see at Anchor:

3–6 months behind, simple business: 2–3 weeks. One or two bank accounts, one credit card, no payroll complications, clean records. This is the easy case.

6–12 months behind, moderate complexity: 3–5 weeks. Multiple accounts, payroll involved, some chart of accounts cleanup needed.

12–24 months behind, complex business: 6–10 weeks. Multiple revenue streams, contractors, sales tax in multiple states, possibly multiple entities.

2+ years behind or major restructure: 8–16 weeks. Often involves coordinating with a CPA on amended returns and may require careful, line-by-line reconstruction of records using bank statements and supporting documentation.

The biggest variable isn’t actually the time period — it’s how organized your source documents are and how quickly you can get them to your bookkeeper. A client with three years behind but clean records can be faster to catch up than a client six months behind with missing statements.

How Much Does Catch-Up Bookkeeping Cost in 2026?

Catch-up bookkeeping is typically priced one of three ways:

Per-Month Pricing

Most common. A flat fee per month being caught up, usually $200–$600 per month depending on complexity. A 12-month catch-up at $350/month is $4,200 total.

Hourly

Some bookkeepers charge $75–$150/hour. This can make sense for very simple cleanups, but tends to create budget surprises on complex jobs. Avoid hourly engagements without a written cap.

Project Flat Fee

After a discovery call and review of your records, the bookkeeper quotes a single fixed price for the entire catch-up. This is the most predictable option and what we typically recommend for engagements over six months.

Real Pricing Ranges We See

- Sole proprietor, 6 months behind, one bank account: $1,500–$3,000

- LLC, 12 months behind, 2-3 accounts, no payroll: $3,000–$6,000

- Small business with payroll, 12 months behind: $5,000–$9,000

- Construction or trucking business, 18 months behind: $7,000–$15,000

- Multi-entity or franchise, 24+ months behind: $10,000–$30,000+

Be skeptical of any quote under $1,000 for a real catch-up engagement. That price typically buys you transaction entry without reconciliation, cleanup, or financial statements — which means you’ll be paying someone else to fix it again later.

Why Catch-Up Costs More Than Ongoing Bookkeeping

Business owners are sometimes surprised that catching up 12 months costs more than 12 months of ongoing service would have. There’s a reason:

- No bank feed shortcuts — many older transactions can’t be auto-imported and have to be entered or matched manually

- Memory has faded — you don’t remember what that $4,200 transfer was for last August, and reconstructing the context takes time

- Errors compound — every miscategorized transaction in month 1 has to be untangled before month 12 makes sense

- Source documents are scattered — receipts in email, statements in three different bank portals, contractor invoices in a shoebox

- More questions, slower answers — your bookkeeper has to ask you about old transactions, and you have to find time to answer

This is why catch-up gets exponentially more expensive the longer you wait. Six months behind is a project. Three years behind is a much bigger one.

What Happens If You Don’t Catch Up?

It’s tempting to keep pushing this off, especially if the business is profitable and the bank account looks healthy. The actual costs of staying behind:

- Missed tax deductions — without clean books, you can’t substantiate expenses, and most businesses behind on books overpay taxes by 8–15%

- Late filing penalties — IRS penalties for late tax filings start at 5% per month of unpaid taxes and can reach 25%, plus interest

- Failed loan applications — banks and SBA lenders require current financial statements to underwrite loans, and “we’ll have them next month” doesn’t qualify

- Business decisions made on bad data — pricing, hiring, expansion decisions made off the bank balance instead of real financials are how businesses quietly lose money

- Increased audit risk — IRS audits are more painful (and more expensive to defend) when you have years of disorganized records

- Lost equity if you sell — buyers and investors discount valuations heavily when due diligence reveals years of unreconciled books

For most businesses, catch-up bookkeeping pays for itself within the first year through tax savings alone.

How to Choose a Catch-Up Bookkeeper

Not every bookkeeper is good at catch-up work. The skills that make someone great at ongoing monthly bookkeeping (consistency, attention to detail) are different from the skills that make someone great at catch-up (investigation, problem-solving, and comfort with messy data).

Questions to ask before hiring:

- How many catch-up engagements have you completed in the past year? Look for at least 10–15. This work is a specialty.

- What does your discovery process look like? Anyone who quotes you without seeing your records is guessing.

- Will the work be done by you or someone on your team? Get clarity on who’s actually doing the work and what their experience is.

- How do you handle reconciliation? If they don’t reconcile every account every month, walk away.

- What deliverables do I get at the end? You should receive month-by-month financial statements, a reconciled QuickBooks file, and documentation.

- What happens after catch-up? Will they roll you into ongoing service, or hand you off cleanly? Either is fine — but you want a plan.

- Do you work with a CPA, or am I responsible for that handoff? Coordination matters when amended returns are involved.

Frequently Asked Questions

How far back can I catch up my bookkeeping?

There’s no technical limit, but most catch-up engagements go back 1–3 years. The IRS generally recommends keeping records for at least 7 years, and amended returns can be filed up to 3 years after the original filing date in most cases. If you’re more than 3 years behind, you’ll likely also need to coordinate with a tax professional on past returns.

Can I just start fresh and ignore the past?

Generally no — and definitely not if you have outstanding tax filings, loans, or business partners. “Starting fresh” leaves your prior tax filings unsupportable in an audit, and any future financial statements will be useless without an accurate beginning balance. The exception is some sole proprietors with very simple businesses who are just changing entity types.

Will catch-up bookkeeping trigger an IRS audit?

No — getting your books in order doesn’t increase audit risk. If anything, it decreases it, because you’ll have the documentation to defend your filings. What can trigger an audit is filing inconsistent or wildly wrong returns, which is more likely without clean books.

Should I do catch-up bookkeeping myself to save money?

If you’re 2–3 months behind on a simple business, possibly yes. If you’re 12+ months behind, almost never — the time you’ll spend untangling past mistakes is better spent on revenue-generating work, and DIY catch-up commonly introduces new errors that need to be cleaned up later. The math rarely works out in favor of DIY for engagements over six months behind.

Can I do catch-up in QuickBooks Online?

Yes. QuickBooks Online handles catch-up well, especially when bank feeds reach back at least 90 days (most banks now provide 12–24 months of history through QBO). For older periods, transactions are entered manually from statements. Catch-up is also possible in QuickBooks Desktop, Xero, and Wave, with similar process.

Will I need to file amended tax returns?

Sometimes. If your prior tax returns were filed using inaccurate financial data, your CPA may recommend amended returns to claim missed deductions or correct errors. Most catch-up clients we work with end up filing 0–2 amended returns. The decision to amend is always made jointly with a tax professional based on materiality and statute of limitations.

How do I prepare for catch-up bookkeeping?

The biggest things you can do to speed up the process: gather every bank and credit card statement for the catch-up period, locate prior tax returns, list all software subscriptions and recurring vendors, write down anything unusual about specific transactions you remember, and provide read-only access to bank accounts through QuickBooks Online if possible. Good preparation can cut catch-up time and cost by 20–30%.

Ready to Get Caught Up?

At Anchor Bookkeeping, catch-up is one of the things we do most. We’ve cleaned up books for construction companies 18 months behind, law firms with three years of unreconciled trust accounts, trucking companies with a shoebox of receipts, and sole proprietors who just want a clean start. As QuickBooks Platinum ProAdvisors based in Charlotte, NC, we provide flat-fee catch-up engagements with clear timelines and no surprises — and we’ll roll you into ongoing monthly service so you don’t end up here again.

→ Schedule a free catch-up consultation

About the Author

Jenny Rodriguez is the Founder & CEO of Anchor Bookkeeping & Tax Solutions, based in Charlotte, NC. With over 10 years of experience supporting construction, trucking, legal, and real estate businesses, Jenny is a QuickBooks Platinum ProAdvisor and bilingual financial professional (English/Spanish). She founded Anchor in 2016 to give growing businesses the financial clarity and proactive support they deserve.

Browse Resources by Topic

Reach Out for Expert Guidance

Contact Anchor Bookkeeping and Tax Solutions today for tailored support in managing your financial needs. Our team is ready to provide personalized assistance to help you achieve your financial goals.